Business loan payback periods and ROI are related because the payback period influences the total cost of the loan and how much the monthly payment is, which impacts a company’s cash flows.

The ROI from a business loan comes from this equation:

- ROI = (Return – Cost) / Cost

With this said, a full and detailed analysis will be a bit different. Comparing loans with different time horizons can be more accurate by using Net Present Value (NPV) or an Internal Rate of Return (IRR) analysis. These account for the “time value” of money. Saving one dollar in month 1 can be worth more than a dollar saved in month 60. At the end of the post, you’ll find a spreadsheet and formula you can use that helps with a clearer picture.

Payback periods influence both the return and the cost in this equation. They impact the return by giving the business owner more/less cash flow each month to put into other parts of the business and they impact the cost primarily through how much interest expense a company pays on the loan.

Business loans with longer payback periods cost more in interest but have lower monthly payments. A lender might offer you a $100K equipment financing loan for 5 years at 10%, or 10 years at 14%. You’d pay $2,121 per month and $27,260 total interest for the shorter term and $1,553 per month and $86,360 total in interest for the longer payback period. The longer loan is more than 3 times the interest cost but the lower monthly payments might make it affordable when the shorter term isn’t an option.

Payback periods on short-term business loans have the same relationship between payback period and ROI. A 6-month $30,000 working capital loan at 20% costs $1,774 in interest with a monthly payment of $5,296. A 2-year option at 25% costs $8,427 but the monthly payment is $1,601. The longer payback period makes the loan cost increase more than 4 times, but the ROI depends on how you reinvest the difference in monthly payments.

Whether a longer or shorter payback period produces a better ROI for your business depends on your specific situation, investment, details of the loan, and what options you have to reinvest cash if you take a longer payback period. To determine whether a longer payback period will help or hurt your business loan ROI, first figure out the difference in cost across loan options.

How Payback Periods Impact the Cost of Total Investment

Payback periods impact ROI through the total interest expense that’s higher for longer periods. For the same loan purpose, lenders charge higher interest rates for longer payback periods both to offset the higher default risk and to account for the cost of having funds tied up longer.

How much more you’ll have to pay depends on your business credit score, the purpose of the loan, the difference in loan terms, and your lender’s internal risk guidelines. Here’s an example to demonstrate comparing $100,000 business loan options.

| Term | Rate | Payment | Total Paid | Total Interest |

| 5 years | 10% | $2,121 | $127,260 | $27,260 |

| 7 years | 10% | $1,660 | $139,440 | $39,440 |

| 10 years | 10% | $1,321 | $158,520 | $58,520 |

| 7 years | 12% | $1,764 | $148,176 | $48,176 |

| 10 years | 14% | $1,553 | $186,360 | $86,360 |

By increasing the payback period you increase the total cost of the investment even if the interest rate were the same. More likely, you’ll pay a higher interest rate for a longer payback period like you see going from a 5-year at 10% to 10-year at 14%, which increases total interest expense for your investment by $59,100.

While this increases the cost portion from the earlier ROI equation, you next need to determine if you can reinvest the difference in monthly payments to see how the longer payback period impacts your overall ROI.

Higher Returns from Longer Payback Periods on Investment Loans

Reinvesting cash from lower monthly payments drives higher ROI only if you can reinvest the cash from lower monthly payments in another investment that will make more than your higher interest expense from the longer payback period. The trick is to do this during the term of the shorter loan option because that’s the only time you have lower payments.

Continuing with the earlier example, the 5-year at 10% versus 10-year at 14% lets you reinvest $563 per month. After 5 years, you wouldn’t have payments on the 5-year loan, which is why you can only think about reinvesting 60 months of $563 cash flow. The question is whether you’re able to invest 60 months of $563 ($33,780 total) to make more than the $59,100 difference in interest expense between the loans.

You would need a consistent 23%+ return on another investment to break even in this example. In other words, unless you can reliably reinvest $563 each month and earn more than 23% annually, the longer payback period will reduce your ROI.

Choosing the Payback Period for Your Loan

Choosing a longer versus shorter payback period normally comes down to whether you can afford the monthly payments. If your investment won’t generate cash immediately, you need free cash from the rest of your business to cover the monthly payments.

SBA 7(a) loans to buy new machines for the factory may not start producing until month 3 after they’re installed and operators are fully trained, but you’ll have to start making payments in month 1. It’s also important to plan for possible shocks to your estimated investment cash flows. If you’re using equipment financing for a new tractor, a drought next year might mean lower yield and less cash flow than normal.

If monthly cash flow isn’t an issue for you, then choosing the payback period depends on the cost difference between your loan options and how you’ll reinvest the cash from lower monthly payments. This is where you calculate the difference in interest expense and any other fees between loan options. From there, you’ll identify where you can reinvest the cash flow from lower monthly payments.

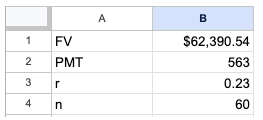

Here’s how to set up a spreadsheet to estimate the total return from reinvestment with the earlier example shown in the image below:

- Put this equation into cell B1: =B2*(((1+B3/12)^B4-1)/(B3/12))

- Enter the monthly payment difference into cell B2

- For where you’ll reinvest the cash flow, put your estimated annual return on investment (“r”) in cell B3. If you generate 50% ROI on inventory and sell out each month, enter .5.

- Enter the length of the shorter loan period in cell B4.

The future value (FV) calculated in cell B1 is your estimated return on the reinvested cash flows. Experiment with different numbers for “r” and make your decision based on how much return you think you’re able to generate versus the extra cost in interest between the loans.

If you can’t put the money to work each month and get a much higher return in the business than you’re paying on the loan, then longer payback periods will most likely lower your business loan ROI since the added costs will outweigh the added return you can generate by reinvesting the monthly payment difference.

Payback period impacts business loan ROI by influencing the total cost of the investment through interest expense and from monthly payment differences that let business owners reinvest cash into the business to generate higher returns overall. Choosing the right payback period depends on whether you have cash flow to cover the monthly payments, and if you do it then depends on your ability to reinvest the cash to drive growth in your business.

National Funding does not provide tax, legal or accounting advice. This material has been prepared for informational purposes only. You should consult your own tax, legal and accounting advisors.