As a small business owner, your dream of expanding, innovating, and running your operations efficiently lies in one critical factor: acquiring the right equipment. Whether you’re a startup or an established company, acquiring heavy machinery, up-to-date technology, or specialized tools is essential.

How Does Heavy Equipment Financing Work?

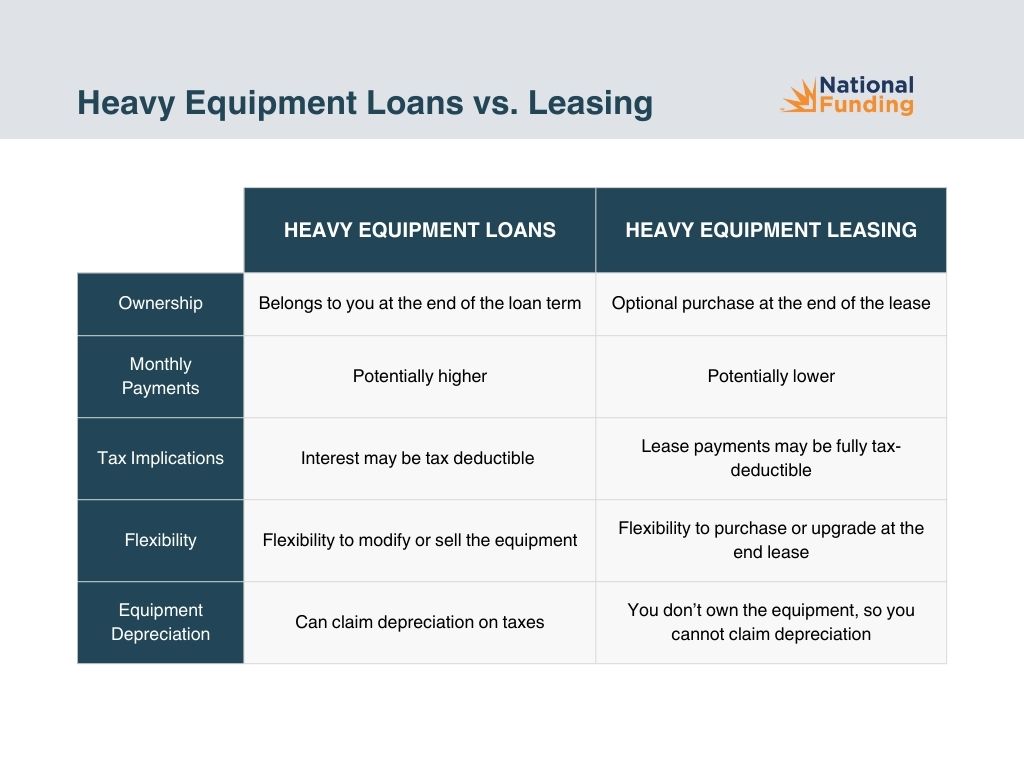

When you need to acquire equipment for your business—whether it’s heavy machinery, vehicles, or technology—you have two primary options: equipment loans and equipment leasing. Both allow you to get the equipment you need without paying the full price upfront.

- Equipment Loans: Equipment loans involve borrowing money to purchase equipment. The lender provides you with a lump sum, which you use to buy the equipment outright. The equipment itself serves as collateral for the loan. If you default on payments, the lender can repossess the equipment. Interest rates vary based on factors like creditworthiness and the type of equipment. Lower credit scores may result in higher interest rates. You’ll typically need to make a down payment (usually a percentage of the equipment’s cost) upfront.

- Equipment Leasing: Leasing involves renting the equipment for an agreed upon time (typically 2–5 years). At the end of the lease, you usually have the option to purchase the equipment. Unlike loans, you don’t own the equipment during the lease term. Leasing may offer tax advantages, as lease payments are often deductible.

Choosing between loans and leases depends on your business needs, cash flow, and long-term goals. Higher interest rates mean higher overall costs. Compare rates from different lenders. A larger down payment reduces the loan amount and lowers monthly payments. Longer terms mean lower monthly payments but potentially higher total interest paid. Consider consulting a financial advisor or funding specialist to make an informed decision.

How to Qualify for a Heavy Equipment Loan?

Most lenders expect your business to be operational for at least one year. This demonstrates stability and reliability. A minimum credit score of around 600 is typically required, although most lenders recommend 650+. A good credit score shows your ability to manage debt responsibly. Lenders often look for annual revenue of at least $250,000. Adequate cash flow ensures you can handle loan payments. You’ll need to make a down payment, usually around 20% of the equipment cost. This shows commitment and reduces the lender’s risk. Heavy equipment loans often use the equipment itself as collateral. If you can’t repay, the lender can seize the equipment.

How to Finance Heavy Equipment

Here’s a concise, step-by-step guide financing heavy equipment:

- Assess your needs and budget accordingly: Understand the specific equipment you require for your business operations. Determine your budget by considering the total cost of the equipment, including taxes, fees, and any additional expenses.

- Research different financing options: Explore all equipment financing options like loans, leasing, rent-to-own options, vendor financing, and government programs.

- Apply to multiple lenders: Submit applications to different lenders to increase your chances of approval. Once approved, review the offers carefully. Compare the repayment terms, interest rates, and fees offered by different lenders.

- Close the loan and acquire equipment: Select the financing option that aligns with your business needs and financial situation. Finalize the paperwork with the chosen lender to acquire the equipment so you can put it to work for your business.

Where to Get Financing

When it comes to financing heavy equipment, specialized lenders focus on this niche. The most common options include traditional banks, online lenders, and the Small Business Administration (SBA). These institutions offer loans and leases tailored to business equipment needs.

1. Small Business Administration (SBA)

The U.S. Small Business Administration (SBA) acts as a co-signer for small businesses seeking loans. The SBA guarantees loans, which means that if a business can’t repay the loan, the government steps in to cover part of the cost. This makes lenders more willing to approve loans for small businesses because they face less risk on their part. Two key SBA loan programs for equipment financing are:

7(a) Loans: These cover working capital and fixed assets (like equipment). Amounts range from $500 to $5.5 million.

504 Loans: These offer long-term, fixed-rate financing through community-based SBA Certified Development Companies; ideal for business growth and real estate purchases.

2. Traditional Banks

When seeking financing for equipment, one of the first places small business owners explore are traditional banks. Let’s explore the pros and cons of this option:

Advantages:

- Traditional banks often have longstanding relationships with local businesses. Building a rapport with your banker can lead to personalized service and better understanding of your needs.

- Banks typically offer lower interest rates compared to other lenders.

- Bank loans come with fixed repayment terms, making it easier to budget and plan payments.

- Consistent repayment on a bank loan can positively impact your business credit score.

Disadvantages:

- Banks have rigorous criteria for loan approval. You’ll need excellent credit, a solid business history, and collateral. Due to the strict requirements, bank loans have a lower approval rate.

- Bank loan applications involve heavy paperwork and thorough evaluation. This process can be time-consuming.

- Banks may take longer to disburse funds compared to online lenders.

3. Online Lenders

Online lenders offer small business owners convenience, speed, and flexibility. Applying online is straightforward.

- You are able to complete the forms from anywhere at any time without having to visit a physical location.

- Online lenders process applications faster than traditional banks. You can receive funds within days (which is crucial for urgent equipment purchases).

- Unlike banks, online lenders are more flexible considering factors beyond credit scores, such as business performance and cash flow.

- Online platforms like SmallBusinessLoans.com can connect you to multiple lenders with just one form, increasing your chances of finding a suitable loan. Whether it’s term loans, lines of credit, or invoice financing, you’ll have choices.

Online lenders usually look for:

- A decent credit score (above 625)

- At least 6 months in business

- $250,000 in gross annual sales

How To Find the Right Equipment Financing For You

When evaluating lenders, consider the following:

- Interest Rates: Understand whether the rate is fixed (consistent) or variable (subject to change based on market conditions). Your credit score, loan term, and market/economic conditions influence the interest rate.

- Repayment Terms: Analyze the period, payment frequency, prepayment penalties, and potential balloon payments.

- Fees/Charges: Understand the additional costs beyond interest, such as origination fees, closing costs, and late payment fees.

- Customer Service: Read reviews to research the lender’s reputation for responsiveness, helpfulness, and transparency.

Remember, a thorough evaluation helps you make informed decisions and secure financing that aligns with your needs and capabilities.

FAQs on Heavy Equipment Financing

Can I Get an Equipment Loan with Bad Credit?

If you have bad credit, there are still options for getting a loan, but they most likely will have higher interest rates and require a cosigner with good credit.

Do I Have to Put Up Collateral?

Equipment loans are usually secured by the equipment itself. However, some lenders may ask for additional collateral so it’s essential to check the specific terms and requirements of each lender to understand what collateral they expect.

What Are the Term Lengths for Financing Heavy Equipment?

The typical term lengths for financing heavy equipment range from 3 to 7 years, however, the exact duration can vary based on the type of equipment you’re financing and the specific lender you choose.